{kind=link}

Jindal Saw Ltd – Total Pipe Solutions

Founded in 1984, Jindal Saw Ltd. has established itself as a market leader in the pipe manufacturing industry, supplying critical infrastructure materials for sectors like oil & gas, water, and industrial engineering. With operations across India, the USA, Europe, and the UAE, the company provides an extensive portfolio ranging from SAW pipes for energy transportation to ductile iron pipes for water management, catering to a global client base of leading oil companies and engineering firms.

Products and Services

- SAW Pipes – Used mainly for oil, gas, and water transportation.

- Ductile Iron & Carbon Alloy Pipes – Serving water transportation and various industries like automotive, power, and process industries.

Subsidiaries: The company operates with 8 direct subsidiaries, 13 indirect subsidiaries, 1 associate, and 1 joint venture as of FY24.

Growth Strategies

- Global Market Reach – Jindal Saw’s strong international presence is supported by a robust order book of $1.65 billion, 32% of which is sourced from global clients.

- Focus on Water & Irrigation – About 70% of current orders are for water and irrigation projects, reinforcing the company’s stronghold in this sector.

- Entry into the U.S. Market – New seamless and stainless products are set to capture U.S. market demand and boost overall margins.

- Infrastructure Investments – The company is enhancing its Mundra coke oven battery for increased electricity generation and improved coal throughput, with Rs.300-350 crore allocated for the project.

- Nashik Plant Expansion – Investing Rs.200 crore to diversify production with new furnaces and larger pipe diameters, increasing capacity by 40-50%.

- Capacity Debottlenecking at Haresamudram – Expansions are expected to elevate ductile iron production to 3 lakh tonnes, making it one of India’s top producers.

- Innovation and Efficiency – Upgrading processes to enhance capacity and efficiency across facilities, strengthening competitive advantage in the market.

Financial Performance

Q2FY25

- Revenue: Rs.5,572 crore (+2% YoY)

- EBITDA: Rs.914 crore (+14% YoY)

- Net Profit: Rs.475 crore (+33% YoY)

FY24

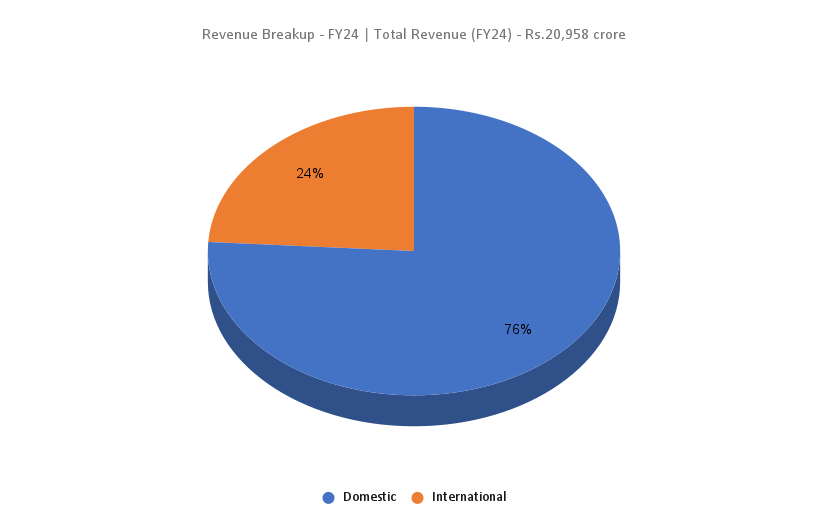

- Revenue: Rs.20,958 crore (+17% YoY)

- Operating Profit: Rs.3,326 crore (+98% YoY)

- Net Profit: Rs.1,593 crore (+252% YoY)

Financial Performance (FY21-24)

- Revenue and Net Profit CAGR: 25% and 71%

- Average ROE & ROCE: 10% and 14%

- Debt-to-Equity Ratio: 0.51

Industry outlook

- Growing Water Demand – India’s development requires extensive water infrastructure for both industrial and domestic needs.

- Government Initiatives – Investment in projects like irrigation, river purification, and the AMRUT-2.0 scheme drives demand for water transmission solutions.

- Pipeline Expansion – Plans to increase pipeline coverage by 54% to 34,500 km by 2024-25.

- Energy Demand Surge – Economic growth is fueling the need for improved energy transport infrastructure.

- Wastewater Infrastructure – Rising sewage generation at a 4.7% CAGR underscores the need for advanced wastewater systems.

Growth Drivers

- FDI Incentives – 100% FDI permitted in oil, gas, and related infrastructure.

- Pipeline-based Irrigation – Adoption in various states, supporting water conservation.

- Urban Water Schemes – Initiatives like AMRUT-2.0 and Smart City to boost demand.

- Infrastructure Investments – Expansion in natural gas and water pipelines.

Competitive Advantage

Jindal Saw’s stable revenue growth and consistent returns make it undervalued compared to peers like Jai Balaji Industries and Venus Pipes & Tubes.

Outlook

- Strong Order Pipeline – With a $1.6 billion order book, the company’s pipeline includes 70% water and irrigation projects and 25% oil and gas, providing a balanced revenue stream.

- Improved EBITDA Margins – Guidance targets a 19% EBITDA margin as stabilization in steel prices aids profitability.

- New Product Lines – Expanded product offerings and entry into new segments position Jindal Saw for sustained growth.

- Export Growth Strategy – Aiming to increase export revenue to 20-25%, up from the current 12%.

- Parent Company Support – The O.P. Jindal Group’s backing provides financial and strategic strength to fuel further growth.

- Efficiency and Capacity Gains – Debottlenecking and expansion initiatives across plants will drive operational efficiencies and production capacity.

- Long-term Growth Potential – These strategic moves underscore Jindal Saw’s commitment to capturing emerging opportunities in infrastructure and industrial segments globally.

Valuation

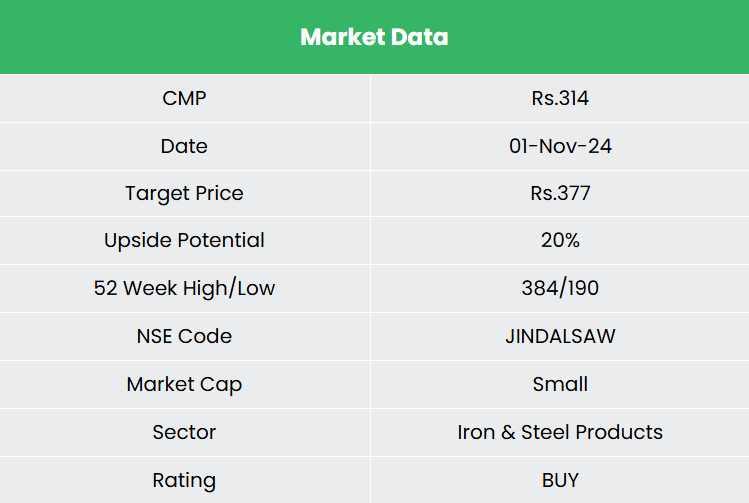

We recommend a BUY with a target price of Rs.377 (12x FY26E EPS), backed by solid fundamentals and growth initiatives.

Risks

- Geopolitical Instability – Possible supply chain disruptions affecting operations.

- Market Competition – New entrants in the DI pipes market could impact market share.

Note: Please note that this is not a recommendation and is intended only for educational purposes. So, kindly consult your financial advisor before investing.

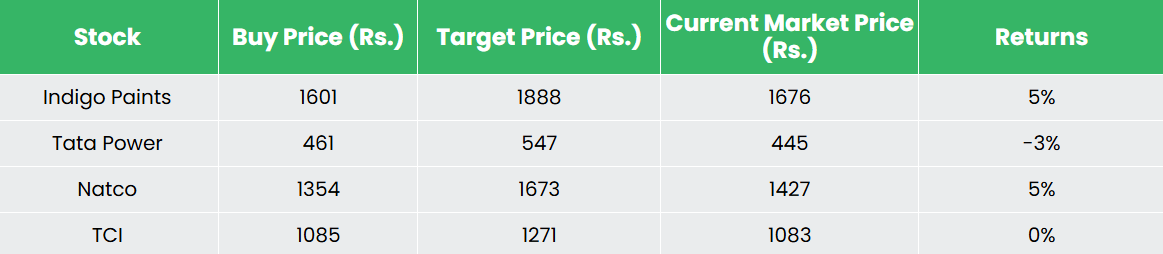

Recap of our previous recommendations (As on 01 November 2024)

Transport Corporation of India Ltd

Other articles you may like

Post Views:

70